Bonjour mes amis! Ever felt like your marriage contract was a bit... vanilla? Like it was missing that certain je ne sais quoi? Well, grab your beret and your best bottle of Beaujolais, because we're about to dive headfirst into the gloriously complex and, dare I say, slightly bonkers world of the Communauté Universelle Avec Clause D'Attribution Intégrale. Try saying that three times fast after a glass of wine!

Now, I know what you're thinking: "What in the Moulin Rouge is that?!" Fear not, my dears, because I'm here to break it down for you, with all the charm and wit I can muster. Think of me as your friendly neighborhood translator, turning legalese into something a bit more... palatable.

Let's start with the basics. The Communauté Universelle, or "universal community," is a marital property regime in France (and some other lucky places, like Quebec) where pretty much everything you and your spouse own becomes communal property. I'm talking your bank accounts, your houses, your slightly embarrassing collection of porcelain dolls... the whole shebang! Think of it as a gigantic, marital piggy bank that you both share. Sounds cozy, right?

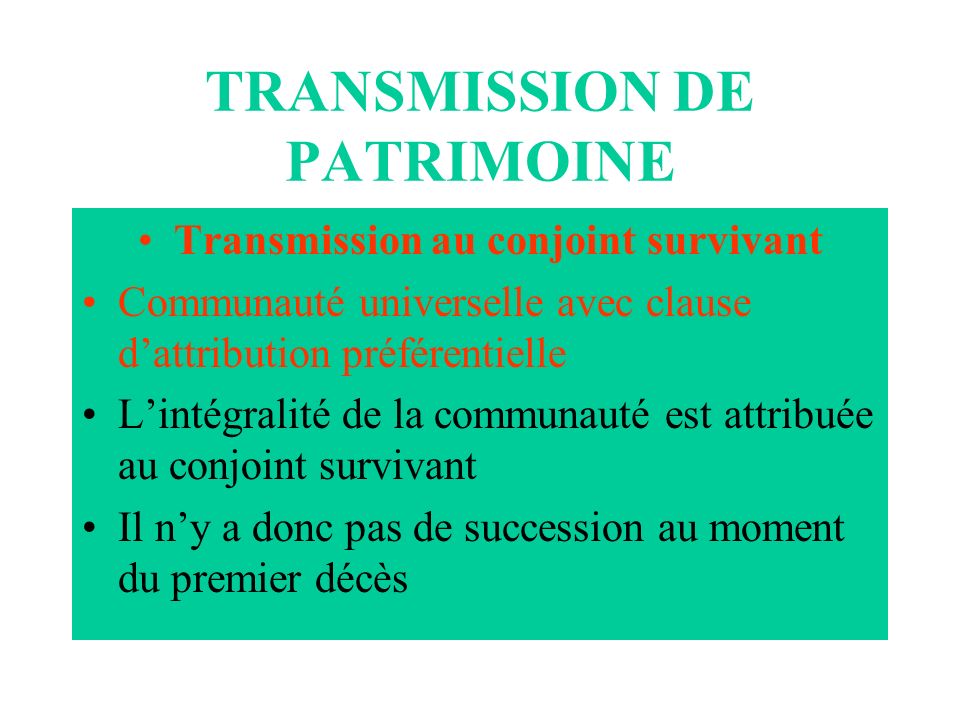

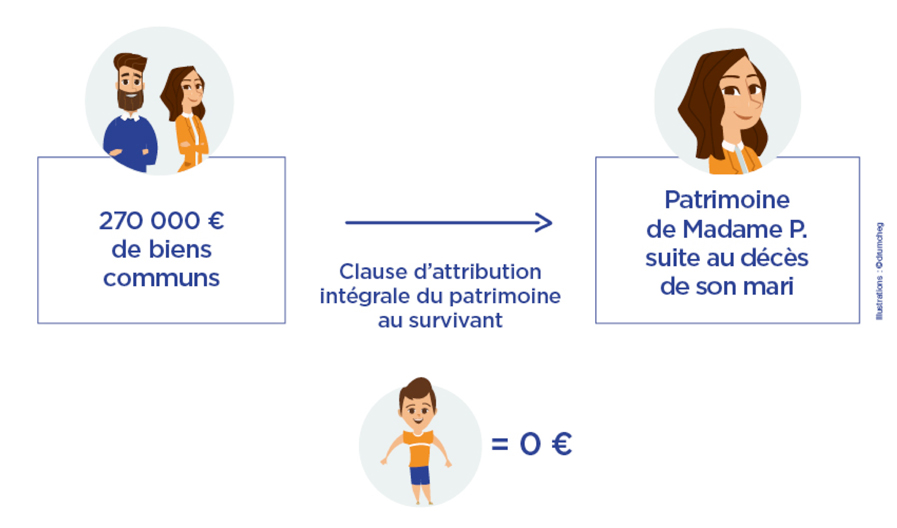

But wait, there's more! That's where the "Clause D'Attribution Intégrale," or "clause of full attribution," comes in. This is where things get really interesting. This clause dictates what happens to that giant, marital piggy bank when one of you, shall we say, kicks the bucket. Instead of the usual inheritance rigmarole, everything goes directly to the surviving spouse. Zip. Zero. Nada for the kids (initially, at least)!

So, What's the Big Deal?

Okay, so you might be scratching your head, thinking, "Why would anyone do that?" Well, there are actually a few compelling reasons, even if they do sound a little extreme at first glance.

- Protection for the Surviving Spouse: This is the biggest one. Imagine a scenario where one spouse owns a business and the other has always been a stay-at-home parent. Without this clause, the surviving spouse could be left in a very vulnerable position, potentially having to sell assets to pay inheritance taxes or even losing the family home. This clause ensures that the surviving spouse is completely taken care of, with no financial worries.

- Simplicity and Efficiency: Let's be honest, inheritance can be a messy, drawn-out affair. With this clause, there's no need for a complicated probate process. Everything is transferred automatically to the surviving spouse, making things much easier during a difficult time. Think of it as the express lane for inheritance!

- Tax Advantages (Potentially): Depending on the specific circumstances and local tax laws, this clause can sometimes offer tax advantages. However, it's crucial to consult with a tax professional to see if it's the right fit for your situation. Don't just assume it's a tax-free ticket to paradise!

The Fine Print (Because There's Always Fine Print!)

Now, before you rush off to your notary with visions of marital bliss and tax-free inheritances dancing in your head, let's talk about the downsides. Because, let's face it, there are always downsides, aren't there?

Potential Problems for the Heirs

This is the big one. As I mentioned earlier, the kids (or other potential heirs) don't inherit anything immediately. Everything goes to the surviving spouse. This can be a problem if:

- There are children from a previous marriage: This is where things can get particularly tricky. The children from the previous marriage could feel completely disinherited, leading to family drama and potential legal battles. Nobody wants that at Thanksgiving dinner!

- The surviving spouse remarries: If the surviving spouse remarries and then dies, the assets could end up going to the new spouse, leaving the original children with nothing. Talk about a plot twist!

- The surviving spouse isn't financially responsible: Let's be honest, we all know someone who isn't exactly a financial whiz. If the surviving spouse isn't good with money, they could squander the inheritance, leaving nothing for the children in the long run.

Loss of Control

Once you enter into a Communauté Universelle, you lose a significant amount of control over your individual assets. Everything is communal, meaning your spouse has just as much right to it as you do. This can be a problem if:

- You have a business you want to keep separate: If you own a business and want to keep it separate from your marriage, this regime is definitely not for you. Your spouse will automatically own half of it!

- You have significant pre-marital assets: If you come into the marriage with a substantial amount of assets, you might not want to commingle them with your spouse's assets.

- You're just generally a control freak: Hey, no judgment! But if you like to be in charge of your finances, this regime might not be the best fit for your personality.

Debt Liabilities

Remember that giant, marital piggy bank? Well, that also means you're both responsible for each other's debts. If your spouse runs up a massive credit card bill, you're on the hook for it! This is something to seriously consider before jumping into a Communauté Universelle.

Is It Right for You? Asking the Important Questions

So, how do you know if the Communauté Universelle Avec Clause D'Attribution Intégrale is right for you? Well, here are a few questions to ask yourselves:

How Strong Is Your Relationship?

This might seem obvious, but it's worth stating explicitly. This regime requires a very high level of trust and communication. You need to be completely open and honest with each other about your finances, your goals, and your fears. If you have any doubts about your relationship, this is probably not the right path for you.

What Are Your Family Dynamics Like?

Do you have children from previous marriages? Do you have a complicated family history? Are there any potential for conflicts among your heirs? These are all important questions to consider. If you foresee potential problems, you might want to explore other options.

What Are Your Financial Goals?

What do you want to achieve financially as a couple? Do you want to protect your assets for future generations? Do you want to simplify your estate planning? Your answers to these questions will help you determine if this regime aligns with your goals.

Are You Willing to Give Up Control?

Are you comfortable sharing control of your assets with your spouse? Are you willing to be responsible for their debts? If you're not, this regime is probably not for you.

Modifying the Beast: Taming the Clause D'Attribution Intégrale

Okay, so maybe the full-blown Clause D'Attribution Intégrale sounds a bit too intense for your liking. Good news! It's not an all-or-nothing deal. You can actually modify it to make it a bit more palatable. Think of it as adding a pinch of salt to your crème brûlée – just enough to enhance the flavor without overpowering it.

Limiting the Scope

One option is to limit the scope of the clause. For example, you could specify that only certain assets are subject to the full attribution. Maybe you want to protect the family home for the surviving spouse, but you want your business to go directly to your children. You can tailor the clause to fit your specific needs and desires.

Adding a Gradual Inheritance

Another option is to add a gradual inheritance provision. This would allow the surviving spouse to inherit the assets immediately, but it would also guarantee that the children (or other heirs) would eventually receive a portion of the inheritance, either upon the surviving spouse's death or after a certain period of time. This can provide a good balance between protecting the surviving spouse and ensuring that the children are taken care of.

Using a Usufruit

Ah, the usufruit! This is a classic French legal concept that allows someone to enjoy the benefits of an asset (like living in a house or receiving income from a property) without actually owning it. You could grant the surviving spouse a usufruit over certain assets, while the children would inherit the nue-propriété (bare ownership). This allows the surviving spouse to continue to enjoy the assets during their lifetime, while also ensuring that the children will eventually inherit them.

The Importance of Professional Advice

I cannot stress this enough: Before you make any decisions about your marital property regime, consult with a qualified notary and a tax professional. This is a complex area of law, and it's easy to make mistakes that could have serious consequences. A notary can help you understand your options, tailor the agreement to your specific needs, and ensure that everything is done legally and correctly. And a tax professional can advise you on the potential tax implications of your choices.

Think of it this way: you wouldn't try to perform surgery on yourself, would you? (Please say no!) Similarly, you shouldn't try to navigate the complexities of marital property law without professional guidance. It's an investment that will pay off in the long run.

Real-Life Scenarios: When It Works (and When It Doesn't)

Let's take a look at a few real-life scenarios to illustrate when the Communauté Universelle Avec Clause D'Attribution Intégrale might be a good idea, and when it might be a recipe for disaster.

Scenario 1: The Loving Couple (It Works!)

Jean-Pierre and Marie have been happily married for 40 years. They have two adult children, both of whom are financially independent. Jean-Pierre owns a small business, and Marie has always been a stay-at-home mother. They have a strong, trusting relationship and they want to ensure that the surviving spouse is completely taken care of, no matter what. In this case, the Communauté Universelle Avec Clause D'Attribution Intégrale could be a good option. It would protect Marie if Jean-Pierre were to die first, and it would simplify the inheritance process.

Scenario 2: The Blended Family (It Doesn't Work!)

Pierre is remarried to Sophie. Pierre has two children from his previous marriage, and Sophie has one child from her previous marriage. Pierre and Sophie are both relatively wealthy, and they each have significant pre-marital assets. In this case, the Communauté Universelle Avec Clause D'Attribution Intégrale would be a terrible idea. It would likely lead to conflict and resentment among the children, and it could potentially disinherit Pierre's children altogether. In this situation, a more tailored marital agreement would be much more appropriate.

Scenario 3: The Business Owner (It Depends!)

Isabelle owns a successful tech startup. She's about to get married to Antoine, who works as a teacher. Isabelle wants to protect her business, but she also wants to ensure that Antoine is taken care of if something happens to her. In this case, the Communauté Universelle Avec Clause D'Attribution Intégrale might be an option, but it would need to be carefully tailored. Isabelle could specify that her business is excluded from the communal property, while still using the clause to protect Antoine's financial security. It all comes down to careful planning and professional advice.

Beyond the Legalese: The Emotional Considerations

It's easy to get bogged down in the legal and financial details of the Communauté Universelle Avec Clause D'Attribution Intégrale. But it's important to remember that this is also an emotional decision. It's about your relationship, your family, and your values.

Think about what's most important to you. Do you want to protect your spouse? Do you want to ensure that your children are taken care of? Do you want to simplify your estate planning? Your answers to these questions will help you make the right decision for your family.

And remember, it's okay to change your mind. You can always modify your marital agreement later on if your circumstances change. The important thing is to have an open and honest conversation with your spouse and to make a decision that you both feel comfortable with.

A Word of Caution (and a Dash of Humor)

Okay, so you've made it this far! Congratulations, you're practically a legal eagle (or at least a very well-informed pigeon). But before you go off and sign on the dotted line, let me leave you with a word of caution:

Don't get swept away by the romance of it all! Yes, the Communauté Universelle Avec Clause D'Attribution Intégrale can sound incredibly romantic – a testament to your unwavering love and commitment. But it's also a very serious legal decision with potentially far-reaching consequences. So, keep your head out of the clouds and your feet firmly on the ground.

And finally, remember that life is unpredictable. You never know what's going to happen tomorrow. So, make sure you have a plan in place, but also be prepared to adapt and adjust as needed. And don't forget to laugh along the way. Because, let's face it, life is too short to be serious all the time!

The Punchline (You Knew It Was Coming!)

So, after all that, are you ready to embrace the Communauté Universelle Avec Clause D'Attribution Intégrale? Well, I hope this little journey has given you a better understanding of what it entails. Just remember, it's not for everyone. But if you're a loving couple who wants to simplify your estate planning and protect the surviving spouse, it could be the perfect fit. Just make sure you consult with a professional first. Otherwise, you might end up accidentally leaving your entire fortune to your spouse's pet hamster. And nobody wants that! Au revoir, and good luck!