Okay, picture this: I was chatting with a friend, let's call him Jean-Pierre (because why not?), who runs a small business importing fancy cheese from, you guessed it, France. He was pulling his hair out, muttering something about bank guarantees and international transactions. Apparently, he almost lost a huge shipment of Roquefort because… well, the details were murky, involving demanding suppliers and hesitant banks. It sounded like a plot from a bad spy movie, except the stakes were really high…like, Brie-high.

Then, in a moment of inspiration (or maybe it was the third glass of wine), I remembered hearing about something called a "Lettre de Crédit Stand By" – basically, a safety net for international business deals. "Jean-Pierre," I said, feeling like a financial guru (which, let's be honest, I'm so not), "have you ever heard of a Standby Letter of Credit?" He looked at me like I'd just recited a line from a Star Trek episode in Klingon. Which, again, I totally could have.

That got me thinking: If Jean-Pierre, a seasoned importer of the world's finest cheese, didn't know about Standby Letters of Credit, then there must be tons of other people out there who could benefit from knowing about this handy financial tool. So, here we are! Let’s demystify this slightly intimidating-sounding thing, shall we?

Qu'est-ce que c'est, une Lettre de Crédit Stand By, anyway?

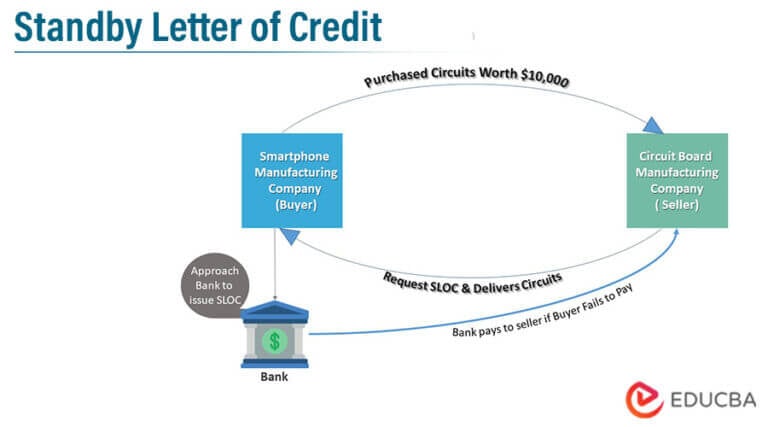

Alright, let's break it down. A Lettre de Crédit Stand By (SBLC), or Standby Letter of Credit, is basically a bank guarantee. Think of it as a promise from a bank to pay a beneficiary (the seller) if their client (the buyer) fails to fulfill their contractual obligations. In Jean-Pierre's case, it would guarantee payment to the French cheese supplier if he, Jean-Pierre, couldn't pay for the Roquefort for some reason (a catastrophic cheese-related incident, perhaps?).

So, it's not really about credit, in the traditional sense. It's more like an insurance policy for a transaction. The bank isn't expecting to pay out, but it's there as a safety net, giving the seller peace of mind and encouraging them to go through with the deal. Think of it as saying, "Hey, I trust my client, but just in case they get abducted by aliens who demand all the cheese, we've got you covered." Dramatic, I know, but you get the picture.

Important Side Note: Don't confuse a Standby Letter of Credit with a Documentary Letter of Credit. They sound similar, but they work differently. A Documentary Letter of Credit is used primarily for payment, with documents presented as proof of shipment. A Standby Letter of Credit is used only as a backup, if the buyer defaults.

Why would you need one?

Good question! There are tons of reasons why a business might need a Standby Letter of Credit. Here are a few of the most common:

- International Trade: Like in Jean-Pierre's case, it's especially useful for international transactions where the buyer and seller don't know each other well and are in different countries. It mitigates risk for both parties. Imagine trying to convince someone in New Zealand to ship you a container full of kiwis without any guarantees. A Standby Letter of Credit could be a game-changer!

- Performance Guarantees: Let's say you're hiring a contractor to build an extension on your house. You could ask them to provide a Standby Letter of Credit guaranteeing they'll complete the work according to the contract. If they don't, you can draw on the letter of credit to cover the costs of hiring someone else to finish the job. (Okay, maybe this is too dramatic for a house extension, but you get the idea.)

- Financial Guarantees: It can be used to guarantee repayment of a loan or other financial obligations. For example, a company might use a Standby Letter of Credit to back up a commercial paper issuance. (Things are getting a bit technical now, aren't they? Don't worry, we're not diving into the deep end.)

- Advance Payment Guarantees: If you're paying a supplier in advance for goods or services, you might want a Standby Letter of Credit to ensure that they deliver as promised. It protects you from losing your money if the supplier goes bankrupt or fails to fulfill their obligations.

Basically, any situation where one party needs assurance that the other party will fulfill their obligations is a good candidate for a Standby Letter of Credit.

How does it work, step-by-step?

Alright, let's walk through the process. It sounds complicated, but it's actually pretty straightforward (sort of!).

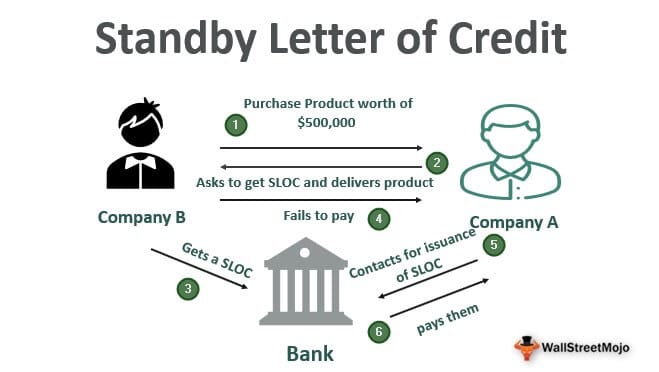

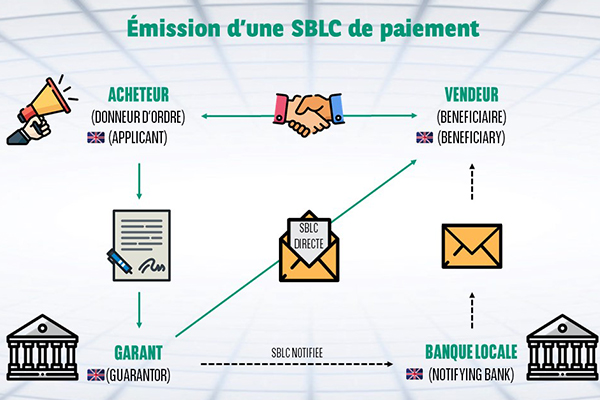

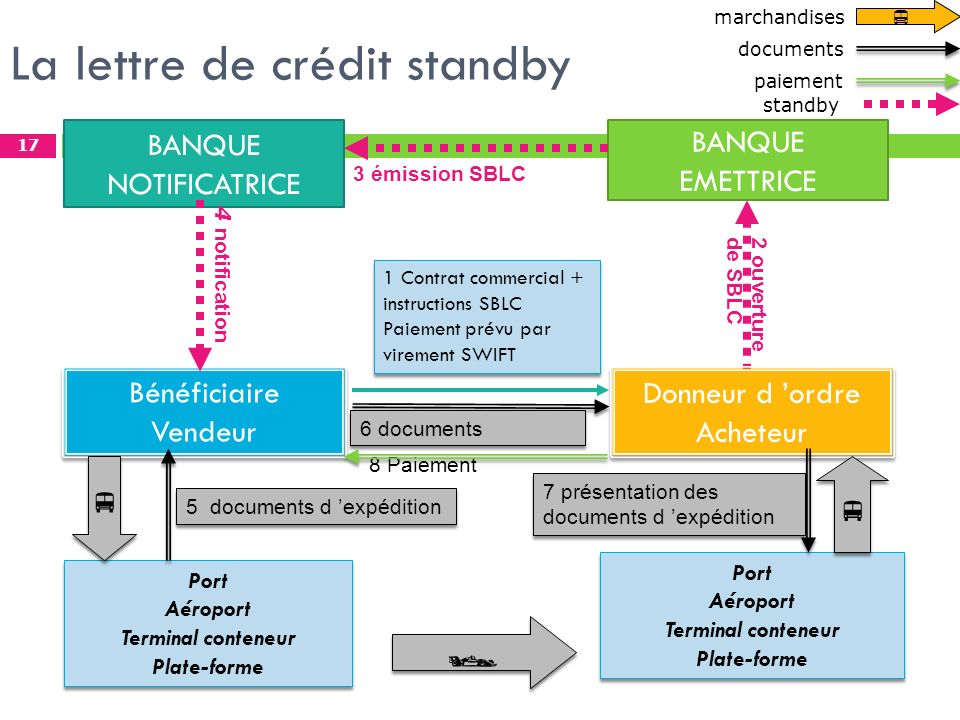

- The Buyer Applies: The buyer (Jean-Pierre, in our cheese example) applies to their bank for a Standby Letter of Credit. They'll need to provide information about the transaction, the beneficiary (the cheese supplier), and the amount of the guarantee. The bank will assess the buyer's creditworthiness and ability to repay. (This is where Jean-Pierre might have to show them his impressive cheese import track record.)

- The Bank Issues the SBLC: If the bank approves the application, they'll issue the Standby Letter of Credit. This is a formal document outlining the terms and conditions of the guarantee. It specifies the amount of the guarantee, the expiry date, and the documents required for drawing on the letter of credit.

- The SBLC is Transmitted: The issuing bank typically sends the Standby Letter of Credit to the beneficiary's bank (the advising bank) in France. The advising bank verifies the authenticity of the letter of credit and forwards it to the beneficiary (the cheese supplier).

- The Beneficiary Feels Secure: The cheese supplier now has the assurance that they'll get paid, even if Jean-Pierre can't pay. They can confidently ship the Roquefort, knowing they're protected.

- The Transaction Proceeds Smoothly (Hopefully!): Jean-Pierre receives the cheese, sells it to his eager customers, and pays the supplier on time. Everyone's happy, and the Standby Letter of Credit sits quietly in the background, never needing to be used. (This is the ideal scenario!)

- If Something Goes Wrong: Let's say Jean-Pierre's cheese shop burns down in a freak fondue accident (knock on wood!). He can't pay the supplier. The supplier then presents the required documents (specified in the SBLC) to the advising bank, proving that Jean-Pierre has defaulted. The advising bank forwards the documents to the issuing bank.

- The Bank Pays Out: The issuing bank reviews the documents. If everything is in order, they pay the supplier the guaranteed amount. The bank then seeks reimbursement from Jean-Pierre.

See? Not too scary. Okay, maybe a little bit scary. But it's a powerful tool for managing risk in international transactions.

The Pros and Cons – because nothing is ever perfect

The Good Stuff:

- Increased Trust: It fosters trust between parties who may not know each other well. This can open up new business opportunities.

- Risk Mitigation: It reduces the risk of non-payment or non-performance. This is especially important in volatile markets or with new business partners.

- Access to Financing: It can help businesses secure financing by providing lenders with added security.

- Competitive Advantage: Offering a Standby Letter of Credit can make you a more attractive business partner, especially in international markets.

The Not-So-Good Stuff:

- Cost: Standby Letters of Credit aren't free. Banks charge fees for issuing and maintaining them. These fees can vary depending on the amount of the guarantee, the creditworthiness of the buyer, and the risk involved. (Think of it as the cost of insurance – you're paying for peace of mind.)

- Complexity: The process can be a bit complex, requiring paperwork and documentation. (But hey, that's why we have banks!)

- Creditworthiness: The buyer needs to have a good credit rating to be approved for a Standby Letter of Credit. (So, make sure you pay your bills on time, Jean-Pierre!)

- Potential for Disputes: Disputes can arise if the beneficiary doesn't comply with the terms and conditions of the letter of credit. (Read the fine print!)

En conclusion...

So, there you have it – a crash course in Standby Letters of Credit. It’s a versatile financial tool that can be a lifesaver for businesses involved in international trade, construction projects, or any other situation where guarantees are needed. While it's not a magic bullet (and definitely not a substitute for due diligence), it can significantly reduce risk and facilitate smoother transactions.

Remember Jean-Pierre and his Roquefort? Well, after our little chat, he actually looked into getting a Standby Letter of Credit. I don't know if he actually got one, but he definitely seemed less stressed about his next shipment. And that, my friends, is a win in my book!

Now, if you'll excuse me, I'm suddenly craving some cheese...

![Tout savoir sur la lettre de crédit stand-by (SBLC) - [Guide Complet 2025]](https://stantax.fr/wp-content/uploads/2019/07/Actionnement-de-la-SBLC-défaillance.png)

![Tout savoir sur la lettre de crédit stand-by (SBLC) - [Guide Complet 2025]](https://stantax.fr/wp-content/uploads/2019/07/mise-en-place-SBLC.png)

.jpg)