Okay, so imagine this. My Aunt Simone, bless her heart, inherited a tiny apartment in Nice. Sea view, you know, the whole shebang. For years, it sat there, mostly empty, occasionally rented to tourists for a hefty price (because, hello, Nice!). Then, boom! She decides to sell. Turns out, Aunt Simone, despite being a whiz at bridge, wasn't exactly up to speed on the tax implications of selling a second property. She thought, "It's mine, I sell, money in the bank!" Oh, Simone...

Which brings me to the juicy topic of première cession d'un logement autre que la résidence principale. Basically, what happens when you sell a property that isn't your main home. Like, say, Aunt Simone's little haven in Nice. Selling a secondary residence is a big deal in France, tax-wise, and it's something you absolutely need to understand before you even think about sticking a "À Vendre" sign in the window. Trust me on this one.

What Exactly is a "Logement Autre que la Résidence Principale"?

Let's break it down. Simply put, it's any property you own that isn't your primary residence. Think:

- Holiday homes (like Aunt Simone's, obviously).

- Rental properties (that apartment you rent out to students near the university).

- A second apartment in the city (because, you know, Parisian chic).

- Even land, in certain cases!

If you sell any of these, you're dealing with the tax implications of a "première cession d'un logement autre que la résidence principale." Now, the "première cession" part is a little misleading. It doesn't mean it has to be the first property you ever sell. It means it's the first time you're selling this specific property. Get it? (I know, French tax law can be a bit like untangling a ball of yarn after a cat's been playing with it.)

So, why is this so important? Well, unlike selling your primary residence (which often comes with certain tax exemptions), selling a secondary property usually triggers a tax on the capital gain (plus-value immobilière). Yep, Uncle Sam (or rather, the French tax authorities) wants a piece of the pie.

Understanding the "Plus-Value Immobilière"

Alright, let's talk about the dreaded plus-value immobilière. This is the difference between the price you bought the property for (your acquisition price) and the price you sold it for (your selling price). If you sell for more than you bought, congratulations! You've made a capital gain. But... (you knew there was a but coming, right?) ...that gain is taxable.

The tax rate is currently around 36.2% in total, comprising income tax (19%) and social security contributions (17.2%). Ouch! That can eat into your profit significantly. This is precisely what gave Aunt Simone a little shock when she learned about it. (She was picturing herself buying a new bridge table with her profits, not handing a chunk of it over to the government.)

Important note: The acquisition price can be increased by certain expenses, like notary fees, agency fees, and the cost of renovations you've made (provided you can prove them with invoices, of course!). So, keep those receipts! They could save you a hefty sum. Think of it as archaeological digging in your old filing cabinets – but with a financial reward!

Exemptions and Reductions: A Glimmer of Hope

Don't despair just yet! While the plus-value immobilière sounds scary, there are some exemptions and reductions that can lessen the blow. The longer you own the property, the lower the tax becomes. The French tax system offers allowances for holding period. After 22 years, you're completely exempt from income tax on the capital gain, and after 30 years, you're completely exempt from social security contributions. So, patience, young Padawan!

Here’s a breakdown:

For Income Tax (19%):

- Years 1 to 5: No reduction

- Years 6 to 21: 6% reduction per year

- Year 22: 4% reduction

- After 22 years: Full exemption

For Social Security Contributions (17.2%):

- Years 1 to 5: No reduction

- Years 6 to 21: 1.65% reduction per year

- Year 22: 1.60% reduction

- Years 23 to 30: 9% reduction per year

- After 30 years: Full exemption

Are you seeing the beauty of long-term real estate investment now? It’s like a slow-cooker recipe for tax savings!

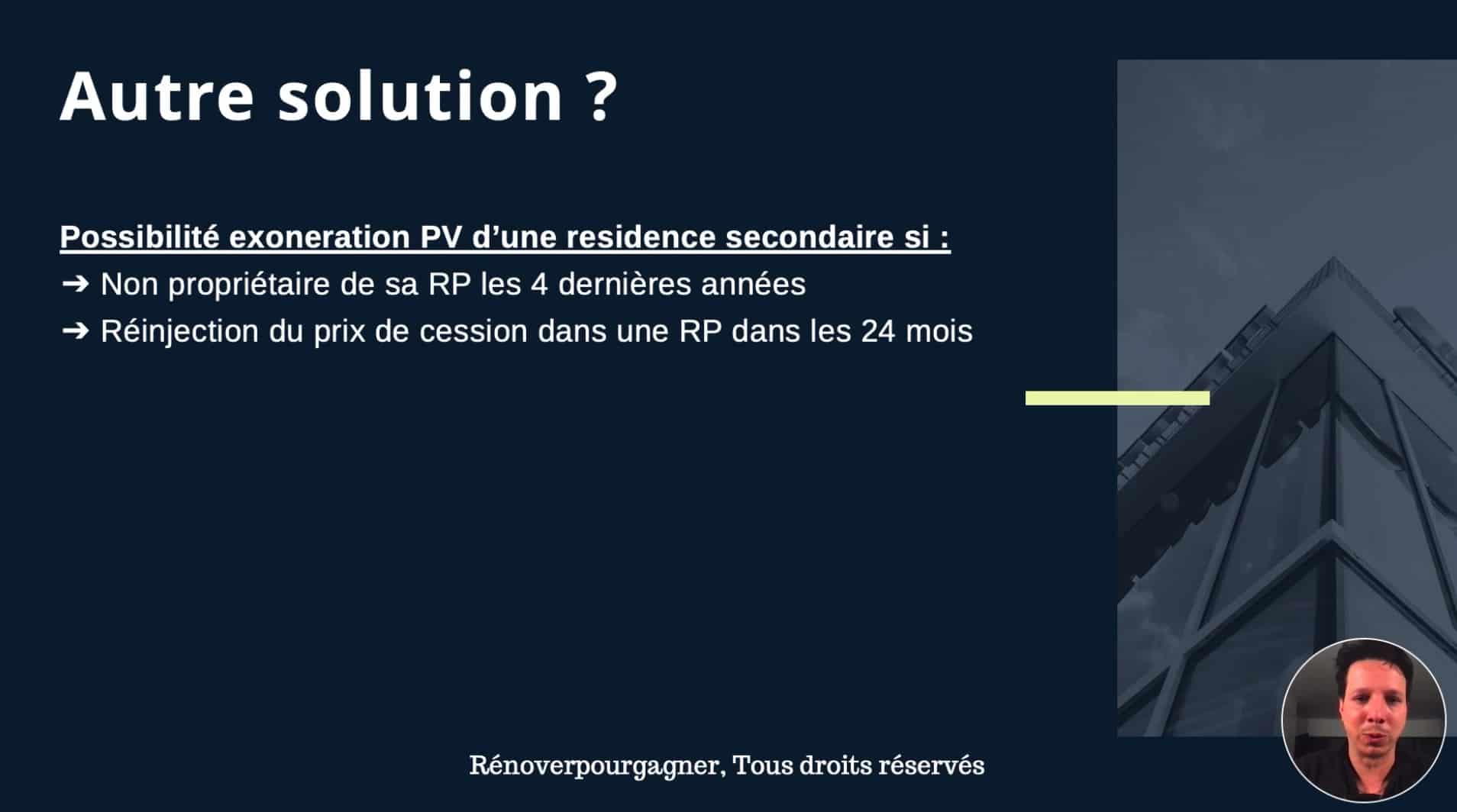

There are also other potential exemptions, such as if you reinvest the proceeds of the sale into buying your primary residence (subject to certain conditions), or if you're selling due to a specific hardship (like a disability or retirement with a low income). These situations are complex and best discussed with a tax advisor. Seriously, don't try to navigate this alone. (Unless you enjoy spending your evenings deciphering complex legal jargon, in which case, more power to you!)

How to Declare and Pay the Tax

When you sell a property, the notary is responsible for calculating the plus-value immobilière and paying the tax to the tax authorities. So, you don't have to worry about filling out complicated forms yourself (thank goodness!). The notary will handle the paperwork as part of the sale process.

However, it's still crucial to provide the notary with all the necessary information, including:

- The original purchase deed.

- Invoices for any renovation work.

- Any other relevant documents that could help reduce the tax.

Think of the notary as your guide through this tax maze. They're there to help you, but they can only work with the information you give them. So, be organized, be prepared, and be ready to answer their questions. And maybe bring them a box of chocolates as a thank you. They'll appreciate it!

Key Takeaways (Because Nobody Likes Reading Walls of Text)

Let's recap, shall we? Selling a secondary residence in France involves understanding the plus-value immobilière, which is the tax on the capital gain you make from the sale. The tax rate is significant, but there are exemptions and reductions based on how long you've owned the property. The notary will handle the tax declaration and payment, but you need to provide them with all the necessary information. And, most importantly, don't underestimate the importance of seeking professional advice from a tax advisor or accountant. Seriously, it’s worth the investment.

Back to Aunt Simone. After she learned about the tax implications (and after a brief period of mild panic), she consulted with a tax advisor. They helped her identify some deductible expenses and ultimately reduced her tax bill. She still had to pay a significant amount, but it was less than she initially feared. And she did get her new bridge table, eventually. The moral of the story? Knowledge is power, and a good tax advisor is your superpower.

So, if you're thinking about selling a secondary property, do your research, seek professional advice, and don't end up like a deer in headlights, like Aunt Simone almost did! Happy selling! (And may your tax bill be as small as possible.)

.png?width=1700&name=residence secondaire airbnb (1).png)