Okay, imagine this: You're at a cocktail party, trying to subtly maneuver away from Brenda who's again telling you about her cat's dietary preferences (seriously, gluten-free for a cat?). You spot someone interesting across the room, a sharp-dressed individual holding court. You sidle over, hoping for a stimulating conversation. And what do you hear? Talk of… renonciation à l'insaisissabilité de la résidence principale. Seriously? Party conversation?

Believe it or not, this legal concept – waiving the protection of your primary residence from creditors – can be surprisingly relevant. It's not exactly the life of the party, granted, but understanding it could save you (or someone you know) from a major headache. And hey, you might even impress Brenda next time!

So, What's All the Fuss About?

Let's break it down. In France (and many other countries), your primary residence is typically protected from being seized by creditors in case of debt. This is thanks to the concept of insaisissabilité – think of it as a legal shield for your home. It's there to prevent you from becoming homeless if you run into financial difficulties.

But, and this is a big but, you can actually choose to waive this protection. You can renoncer, as they say. Why would anyone in their right mind do that? That's the million-dollar question, isn't it?

The 'Why Would I Ever Do That?' Explained

The most common reason to waive this protection is to secure a business loan. Banks and other lenders often demand this as collateral, especially for entrepreneurs or small business owners. They want reassurance that they'll get their money back, even if things go south.

Think of it this way: it's like offering your house as a guarantee. "Hey bank, I'm super confident my business will succeed, but just in case, you can have my house if I default." Sounds risky, right? Because it is!

Here’s a quick list of scenarios where you might encounter this:

- Starting a Business: As mentioned, lenders may require it for business loans.

- Restructuring Existing Debt: You might use your home as collateral to consolidate or renegotiate existing debt.

- Attracting Investors: Waiving the protection could make your business more attractive to investors who want security.

Before we dive deeper, let's be clear: this is a serious decision. It's not like signing up for a gym membership. It has potentially devastating consequences. You are literally putting your home on the line.

The Nitty-Gritty Details: How Does It Work?

Okay, you’ve decided (or are at least considering) this whole renunciation thing. What are the actual steps involved? It's not as simple as scribbling something on a napkin.

Form and Procedure

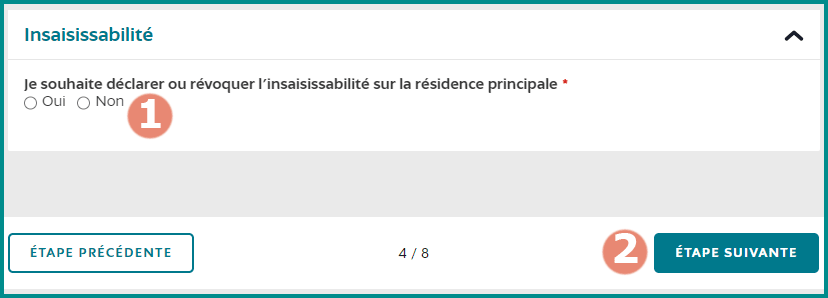

First, the renunciation must be done in writing. You can't just verbally agree to it. It has to be a formal declaration, usually drafted and notarized by a notaire (a French notary public). The notaire plays a crucial role in explaining the implications and ensuring you understand what you're doing. They are legally obligated to advise you. Think of them as the designated voice of reason in this potentially crazy situation.

The declaration must be very specific. It needs to clearly identify the debt it's securing, the amount, and the creditor. It can't be a blanket waiver for all future debts. It's a targeted surgical strike, not a nuclear option. (Okay, maybe it is a nuclear option, but a targeted one!)

What Happens if You Default?

This is where things get real. If you fail to repay the debt according to the agreed terms, the creditor can initiate foreclosure proceedings on your home. This means they can take possession of your property and sell it to recover their money.

The process will involve legal proceedings and potentially a court auction (vente aux enchères). It's a stressful and emotionally draining experience. The idea of losing your home is, understandably, terrifying.

Things to Consider Before You Sign on the Dotted Line

Seriously, before you even think about waiving the protection of your primary residence, ask yourself these questions:

- Is there any other option? Can you secure the loan with other assets? Explore all alternatives before putting your home at risk.

- What's the worst-case scenario? Realistically, what's the likelihood that your business will fail or you'll default on the debt? Don't be overly optimistic. (Entrepreneurs tend to be optimists, which is great, but not when your house is on the line!).

- Have you sought legal and financial advice? Talking to a lawyer and a financial advisor is crucial. They can assess your situation and provide unbiased advice. Don't rely solely on the lender's information.

- Do you truly understand the risks? Make sure you fully grasp the implications of waiving the protection. Don't be afraid to ask questions until you're absolutely certain you understand.

- What are the tax implications? There might be tax consequences associated with this renunciation and potential foreclosure. Consult with a tax professional.

The Notaire: Your Best Friend (and Legal Guardian)

Seriously, can't stress this enough! The notaire is your safeguard in this process. They are there to ensure you understand the legal ramifications and that you're not being taken advantage of. They will explain the document in detail, answer your questions, and advise you on the risks involved.

Don't be afraid to ask them tough questions. It's their job to protect your interests, not the lender's. They are an independent legal professional acting in your best interests.

A Final Word of Caution (Because This is a Big Deal!)

Waiving the protection of your primary residence is a significant decision with potentially life-altering consequences. It should only be considered as a last resort, after exploring all other options. Get professional advice, understand the risks, and proceed with extreme caution. Don't let the allure of a business loan or the pressure from a lender cloud your judgment.

And remember, your home is more than just an asset. It's where you live, where you raise your family, where you build memories. Protect it fiercely.

So, next time you're at a cocktail party and someone brings up renonciation à l'insaisissabilité de la résidence principale, you'll be prepared to have a (slightly less awkward) conversation. And maybe, just maybe, you can steer Brenda away from the cat food discussion entirely!