Okay, imagine this: you're at a massive buffet. Mountains of delicious-looking food everywhere. You pile your plate high, thinking, "Free food! Gotta grab it all!" But then, bam, food poisoning. Turns out, nobody was really checking what was in those dishes, or how long they'd been sitting out. That's kinda like the financial crisis of 2008. Loads of tempting "investments" (the buffet food), and almost zero oversight (the kitchen inspectors on vacation). Scary, right? Well, enter the Dodd-Frank Wall Street Reform and Consumer Protection Act. Think of it as the health inspector for the financial buffet.

What Exactly Is Dodd-Frank, Anyway?

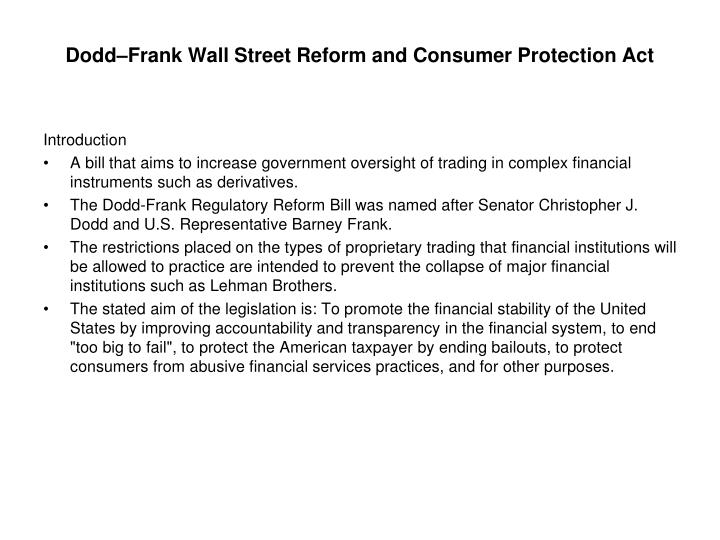

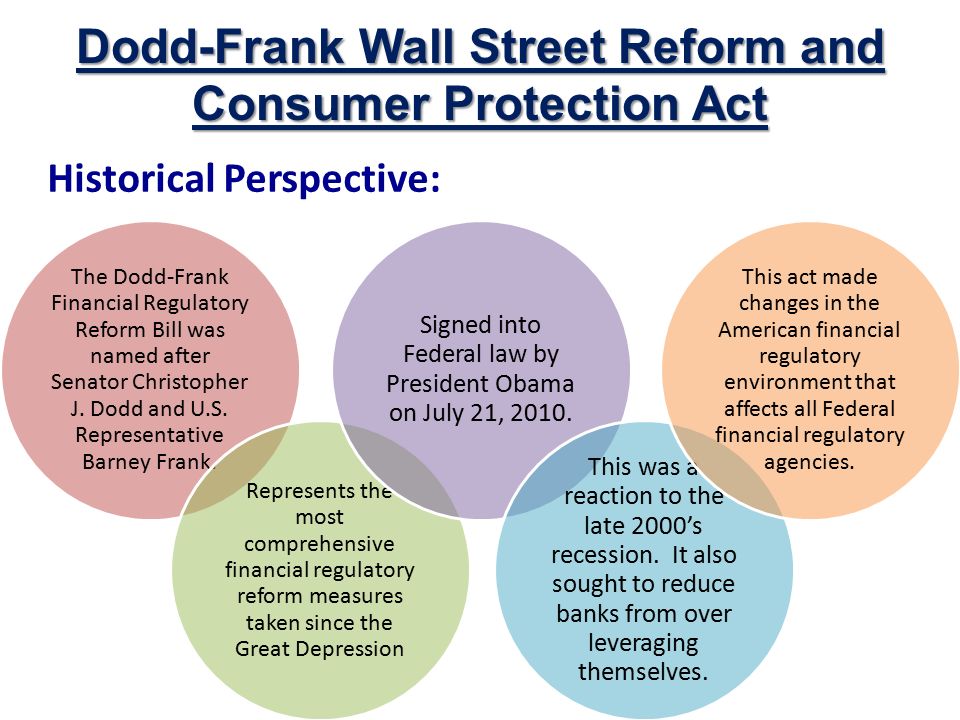

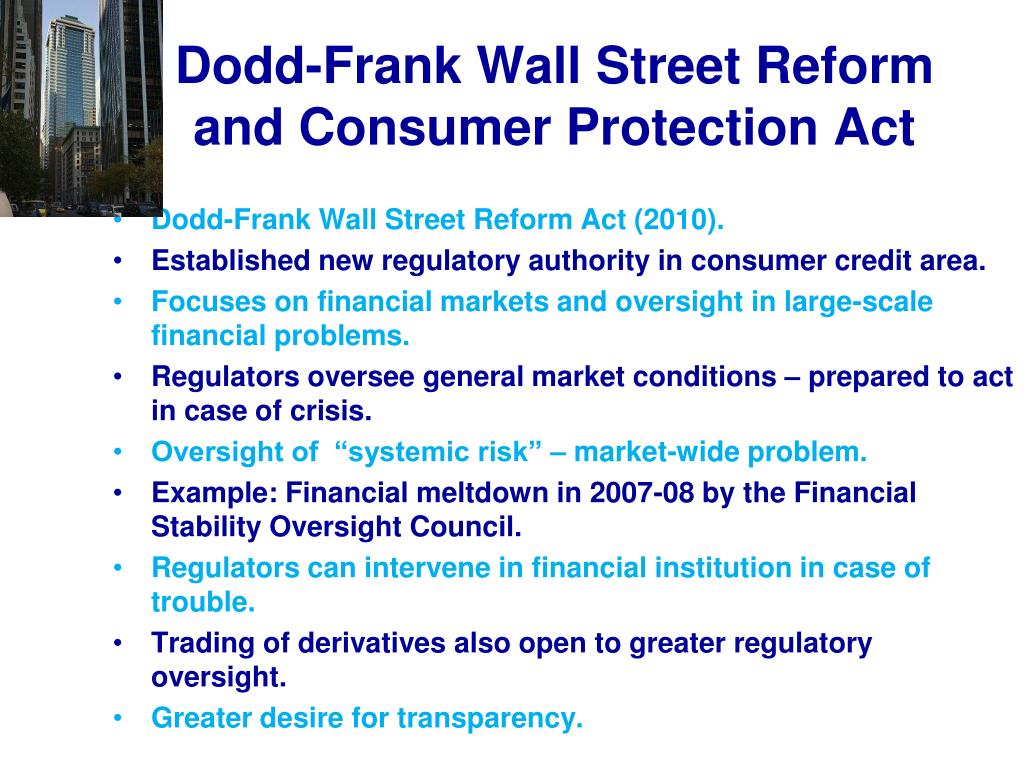

Dodd-Frank, signed into law in 2010, is a massive piece of legislation aimed at preventing another financial meltdown. It's basically a huge rulebook for Wall Street, intended to make the financial system safer and more transparent. Think of it as the fine print you should be reading before diving into any investment. Honestly, it's so dense, even financial experts get headaches trying to decipher it all. But hey, at least someone's trying to make sense of the madness, right?

Why Did We Need It? (A Quick History Lesson)

Remember the housing bubble? Yeah, that wasn't a fun time. Banks were lending money like crazy to people who couldn't afford it, then packaging those dodgy mortgages into complex securities (like financial lasagna – layers upon layers of who-knows-what!). These securities were then sold to investors worldwide. When people started defaulting on their mortgages (surprise!), the whole house of cards collapsed. Banks teetered on the brink of failure, and the government had to step in with massive bailouts. Taxpayer money to the rescue! Again! Dodd-Frank was supposed to prevent that kind of shenanigans from happening again. So, let's delve into some of its key provisions:

Key Components of Dodd-Frank

- The Volcker Rule: This one's interesting. It basically stops banks from using taxpayer-backed deposits to make risky investments for their own profit. Imagine your bank using your savings to gamble on the stock market – not cool, right? The Volcker Rule is meant to separate traditional banking (taking deposits and making loans) from speculative trading. It's like telling the bank, "Hey, stick to the basics, okay?"

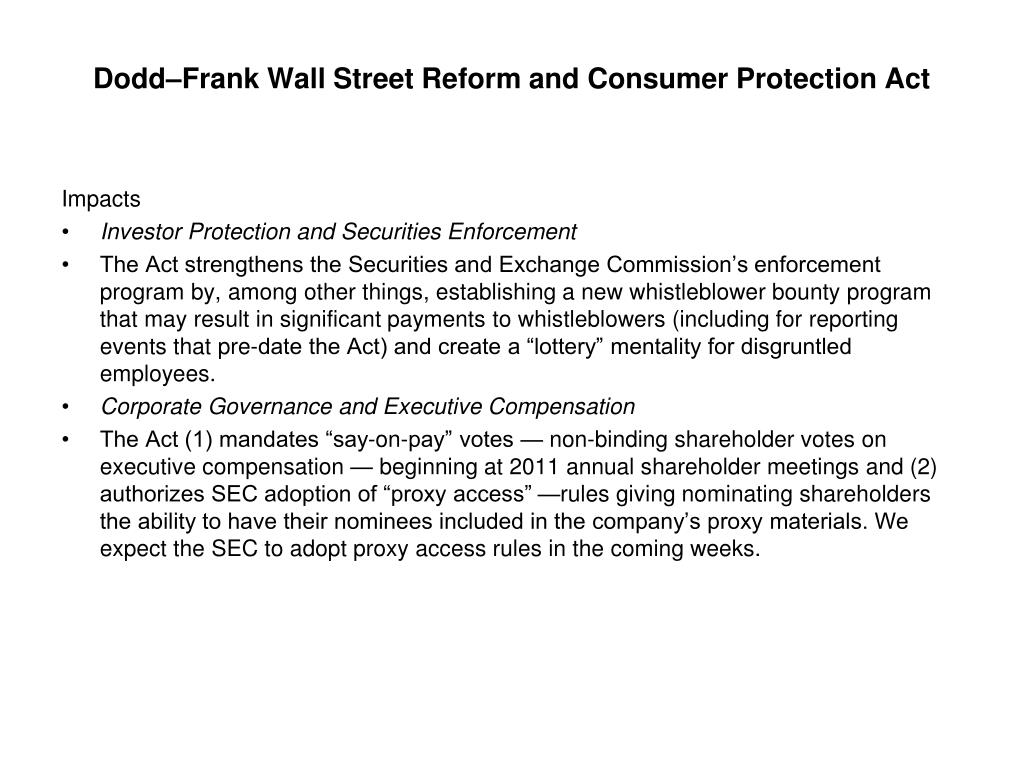

- Consumer Financial Protection Bureau (CFPB): This is a biggie. The CFPB is a government agency specifically designed to protect consumers from financial scams and predatory lending. Think of them as your personal financial watchdog. They investigate complaints, write rules for financial institutions, and generally try to make sure you're not getting ripped off by credit card companies, payday lenders, or mortgage brokers. Good, right? We all need someone watching out for us.

- Oversight of Derivatives: Derivatives are complex financial instruments (we're talking about those financial lasagnas again!), and before Dodd-Frank, they were largely unregulated. The act requires many derivatives to be traded on exchanges and cleared through clearinghouses, which makes them more transparent and reduces the risk of one party defaulting and bringing down the whole system. Transparency is key, folks!

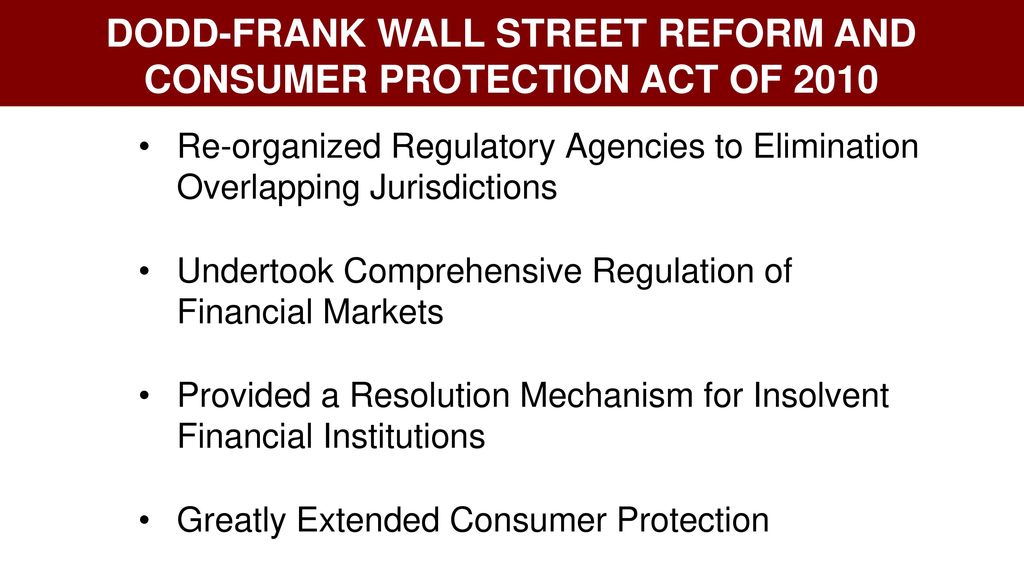

- Systemic Risk Regulation: This is all about identifying and regulating companies that are "too big to fail." These are the companies whose collapse could destabilize the entire financial system. Dodd-Frank gives regulators the power to monitor these companies more closely and require them to hold more capital (basically, a bigger cushion to absorb losses). It's about making sure that if one of these giants stumbles, it doesn't take everyone else down with it. Think of it as a financial airbag for the whole economy.

- Resolution Authority: This gives the government a way to wind down failing financial institutions in an orderly manner, without resorting to taxpayer-funded bailouts. Basically, it's a plan for what to do when a big bank goes belly up. The idea is to protect the financial system without rewarding reckless behavior.

Did Dodd-Frank Actually Work?

Ah, the million-dollar question! That’s debatable, right? Some argue that Dodd-Frank has made the financial system much safer and more stable. They point to the fact that the banking system is better capitalized and more heavily regulated than it was before the crisis. Others argue that the act is overly complex and burdensome, stifling economic growth and innovation. It's like adding so many safety features to a car that it becomes too expensive and slow to drive. Plus, some argue that it hasn't really addressed the underlying causes of the financial crisis, such as excessive risk-taking and moral hazard.

Arguments in Favor of Dodd-Frank

- Increased Financial Stability: Proponents argue that Dodd-Frank has significantly reduced the risk of another financial crisis. The stricter regulations and increased oversight have made the financial system more resilient to shocks. Think of it as building a stronger dam to protect against future floods.

- Consumer Protection: The CFPB has been credited with recovering billions of dollars for consumers who were victims of financial fraud. That's real money going back into people's pockets.

- Greater Transparency: Dodd-Frank has brought more transparency to the financial markets, making it easier to identify and manage risks. Sunlight is the best disinfectant, as they say.

Criticisms of Dodd-Frank

- Complexity and Cost: Critics argue that Dodd-Frank is too complex and costly to implement. The regulations are said to be burdensome for financial institutions, especially smaller banks. It's like trying to navigate a maze with a blindfold on.

- Reduced Lending: Some argue that Dodd-Frank has made it harder for businesses to get loans, hindering economic growth. The tighter regulations are said to have made banks more risk-averse. If you can't borrow money, it's tough to expand your business, right?

- Unintended Consequences: Critics also point to unintended consequences of Dodd-Frank, such as increased concentration in the banking industry. The regulations are said to have favored larger banks, which have the resources to comply with the complex rules. The big fish get bigger, and the small fish get eaten.

Dodd-Frank Today: Is It Still Relevant?

Dodd-Frank has been subject to numerous amendments and revisions since it was enacted. Some parts of the act have been weakened or repealed, while others have been strengthened. The debate over the effectiveness and necessity of Dodd-Frank continues to rage on. It's like a never-ending tug-of-war between those who want more regulation and those who want less.

It's safe to say that Dodd-Frank, while a well-intentioned effort to fix a broken system, hasn’t been a perfect solution. The financial world is incredibly complex and innovative, so regulations often struggle to keep up. It's a constant game of cat and mouse. But hey, at least there is a cat trying to catch the mouse!

Ultimately, the legacy of Dodd-Frank remains to be seen. Will it prevent another financial crisis? Only time will tell. But one thing is certain: the debate over financial regulation will continue for years to come. So next time you hear someone talking about Dodd-Frank, you can at least say you know a little bit about it. And maybe, just maybe, you'll be a little bit more informed about the complex world of finance. Now, who's up for a (carefully inspected) buffet?

.jpg)

:max_bytes(150000):strip_icc()/GettyImages-103014719-e1586f68b3ea4af49c72d346b53e0821.jpg)